Are you offered Company Stock in your 401(k)?

If yes, you may be able to take advantage of a unique tax rule to your benefit when considering retirement distribution strategies. Company stock may be offered through a 401(k) to provide employees with a great opportunity to have a stake in the business while also saving for retirement. Even large organizations that have many shareholders can appreciate the value of aligning corporate and employee efforts through providing company stock in their retirement plans. After many years of accumulating employer stock inside of a qualified plan a time will come when distributions from the plan may make sense. At this time, there are many elements and trade-offs to consider.

A distribution of cash out of the qualified retirement plan account to the account owner will result in recognizing ordinary income by the account owner. From a tax perspective, this is less than desirable. This is especially true if the account holder has been investing in company stock that has appreciated for many years. A key rule, under Internal Revenue Code (IRC) Section 402(e)(4), often referred to as the “Net Unrealized Appreciation” (NUA) can help taxpayers minimize the recognition of ordinary income altogether. At Hudson Oak Wealth Advisory we have experience managing portfolios of employees who have employer stock within their qualified workplace retirement plans and making the most of rules such as NUA.

So What is NUA?

In the simplest terms possible, the potential for NUA is the difference between the original cost (contribution) of employer stock and its present market value.

If the original cost of all contributions into a 401(k) was $250,000 and the current market value is $550,000, the NUA potential is $300,000. This NUA amount may be eligible for significant tax savings.

Certain participants in an employer retirement plan can transfer employer stock out of the plan and into a separate taxable investment account without recognizing the entire distributed amount as ordinary income. This is counter to a normal distribution from a 401(k) which at a minimum are typically entirely taxed as ordinary income (i.e. $1 of distribution = $1 of ordinary taxable income). Under the NUA rules, the previously untaxed contributions of employer stock are treated as any other distribution out of a qualified plan would be treated - creating ordinary income subject to current taxation - but only for the contribution portion (average cost basis); not its entire fair market value.

The NUA in employer stock however avoids current taxation and will receive favorable long-term capital gains tax treatment upon its ultimate sale. Long-term capital gains treatment is afforded regardless of how long the stock was actually held in the plan. Subsequent appreciation of the company stock once it is in the taxable account will also receive capital gains tax treatment.

That’s Great. Are There Other Rules I Should Be Aware Of?

Yes. In order to take full advantage of NUA tax treatment on their company stock, a taxpayer must first meet certain criteria. The plan participant must receive the stock distribution out of the plan as a lump-sum, in-kind distribution pursuant to a “triggering event.” This means the participants needs to transfer the employer stock itself – not cash proceeds – from the employer retirement plan into their taxable investment account. Further, the entire plan balance (company stock and non-company stock holdings) must be distributed out of the participant’s account all in the same tax year. If a single share of employer stock is transferred to a taxable investment account on December 1, 2019, the remainder of all qualified retirement accounts with that employer need to be emptied by December 31, 2019.

A “triggering event” includes death, disability, separation from service or reaching age 59½, and must precede the distribution in order to be eligible for NUA treatment. If a triggering event hasn’t occurred, the appropriate accounts are not emptied in the same tax year, or the stock is not transferred in-kind - NUA treatment is not available. The distribution will receive ordinary income tax treatment.

How About an Example?

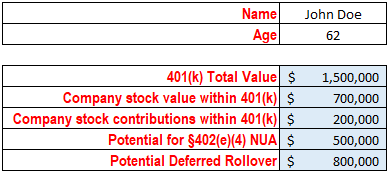

John Doe is 62 years old. He has $700,000 of XYZ company stock in his employer 401(k) with a total balance of $1,500,000 and after a long career at XYZ, decided to retire late in 2018. Of the $700,000 of XYZ stock, $200,000 is from tax-deferred employer stock contributions.

Based on these facts, John has experienced two triggering events that could qualify him for NUA. He is at least 59½ years old and has separated from service. If in 2019 John distributes $700,000 of XYZ stock into his taxable brokerage account, he has until the end of the year to move the remaining $800,000 balance out of the qualified employer retirement account - either as a taxable distribution or potentially as a deferred rollover.

If the NUA approach is desired, the $200,000 of stock contributions is taxable as ordinary income in 2019. While this may be a large amount of ordinary income for John to recognize in one year, the remaining $500,000 of NUA is eligible to avoid ordinary income tax treatment altogether. The stock will receive long-term capital gain treatment when John eventually sells the stock – which is a preferred outcome for John. Any subsequent appreciation of John’s employer stock after he has transferred it to his taxable account will receive either short-term or long-term capital gain treatment.

When does NUA make sense? What are the Planning Considerations of NUA?

It is best to avoid engaging in this strategy too close to year-end. It is not worth the risk of potentially not distributing the entire account in a timely manner and losing the valuable NUA treatment since it must all happen within a single tax year.

The best candidates are often those that have the lowest average cost basis (i.e. amount of employer/company stock contributed) relative to the company stock’s current market value.

Just because all plan assets must be distributed does not mean they must all go into a taxable account. Non-company stock assets can be rolled into a separate tax-deferred retirement plan, avoiding current taxation and maintaining deferred status.

NUA treatment is only available when being transferred out of the original employer’s qualified plan. A taxpayer cannot take advantage of NUA after transferring his company stock from their company’s qualified plan into another 401(k) or IRA. Therefore, if a participant rolls stock into a new employer plan they would not be able to later take advantage of NUA.

NUA is not an “all-or-nothing” proposition. All plan assets must leave employer qualified plans to take advantage of NUA, but participants can select which shares they want to qualify for NUA.

Keep in mind that just because NUA may be available does not mean that other early distribution rules do not apply. If John in our previous example had retired early and was 50 years old, he may qualify for NUA due to his separating from service, however a distribution at that age could result in a 10% early withdrawal penalty on the currently taxable portion.

Unlike like typical capital gains, capital gains from resulting from NUA are not considered investment income for purposes of determining income subject to the 3.8% Medicare surtax or “Net Investment Income Tax”. This is a unique advantage to many since it allows NUA to avoid the ordinary tax treatment of other retirement plan distributions while also avoiding investment income classification when eventually sold. It is important to note however that any post-NUA transfer appreciation of the stock is subject n the 3.8% surtax calculation when it is sold. Taxable distributions from retirement plans can potentially push income over the thresholds for the surtax however.

For heirs that receive company stock in a taxable account that was originally contributed through an NUA transfer, the shares retain the same NUA treatment that existed when the original owner was alive. However, it is important to note that the initial transfer value will not receive a step-up in basis, but subsequent appreciation of the stock after the initial transfer can be stepped-up. Movement in the value of the stock after the initial NUA transfer will dictate whether the ultimate sale will be subject to short and long-term capital gains rates.

What Next?

NUA is a unique opportunity surrounding employer retirement plans and can create powerful tax savings advantages over traditional retirement plan distributions. Careful NUA planning should be part of an overall comprehensive financial plan when applicable. It can unlock savings and improved efficiencies relating to your retirement savings and distribution strategy.

Keep in mind however that the rules can be complex and this strategy is not appropriate for all plan participants that have this available to them. If the rules are not properly followed, a plan participant may jeopardize much of their retirement savings by incurring unnecessary taxes that can erode wealth.

At Hudson Oak we have deep experience working not just with NUA and managing these tax implications but also properly understanding the single stock risk associated with concentrated company stock positions. Before engaging in NUA and other similar retirement plan distribution strategies, we recommend that you consult a qualified tax and financial professional who and can help you navigate these rules and build it into your overall strategic plan.

Disclosure: (“Hudson Oak”) is a registered investment adviser in the State of New Jersey. For information pertaining to Hudson Oak’s registration status, its fees and services and/or a copy of our Form ADV disclosure statement, please contact Hudson Oak. A full description of the firm’s business operations and service offerings is contained in our Disclosure Brochure which appears as Part 2A of Form ADV. Please read the Disclosure Brochure carefully before you invest. This article contains content that is not suitable for everyone and is limited to the dissemination of general information pertaining to Hudson Oak’s Wealth Advisory & Management, Financial Planning and Investment services. Past performance is no guarantee of future results, and there is no guarantee that the views and opinions expressed in this presentation will come to pass. Nothing contained herein should be interpreted as legal, tax or accounting advice nor should it be construed as personalized Wealth Advisory & Management, Financial Planning, Tax, Investing, or other advice. For legal, tax and accounting-related matters, we recommend that you seek the advice of a qualified attorney or accountant. This article is not a substitute for personalized planning from Hudson Oak. The content is current only as of the date on which this article was written. The statements and opinions expressed are subject to change without notice based on changes in the law and other conditions.